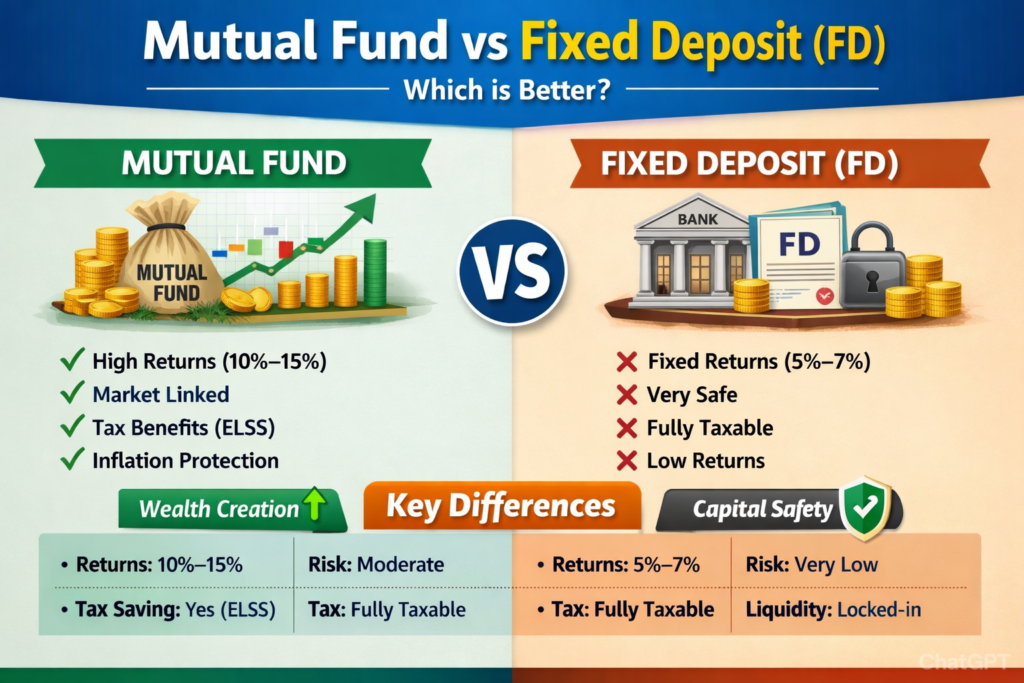

1. Basic Difference

| Feature | Mutual Funds | Fixed Deposits (FD) |

|---|---|---|

| Meaning | Investment in market through fund manager | Money deposited in bank for fixed interest |

| Returns | Market-linked (not fixed) | Fixed and guaranteed |

| Risk | Medium to High | Very Low |

| Returns Potential | 10%–15% average (long term equity) | 5%–7.5% usually |

| Safety | Depends on market | Very safe |

| Lock-in | Usually no lock-in (except ELSS) | Lock-in till maturity |

| Liquidity | Easy to withdraw | Penalty on early withdrawal |

| Taxation | Tax efficient | Fully taxable |

2. Example: ₹10,000 per month for 20 years

| Investment | Approx Value |

|---|---|

| Mutual Fund (12%) | ₹99 Lakhs |

| FD (6%) | ₹46 Lakhs |

👉 Mutual Fund gives more than double returns

3. Who Should Invest in Mutual Funds?

Best for:

✔ Salaried professionals

✔ Long-term wealth creation

✔ Retirement planning

✔ Child education planning

✔ Beating inflation

4. Who Should Invest in FD?

Best for:

✔ Senior citizens

✔ Short-term goals

✔ Emergency fund

✔ Risk-free investors

5. Final Conclusion

👉 FD is for Safety

👉 Mutual Fund is for Wealth Creation

✔ FD grows money slowly

✔ Mutual Fund grows money faster with compounding

6. Best Strategy (Recommended)

Smart investors use both:

• 20% in FD → Safety

• 80% in Mutual Funds → Growth

Fixed Deposits offer safety and guaranteed returns, making them suitable for conservative investors. However, the returns are usually low and may not beat inflation.

Mutual Funds, on the other hand, invest in equity and debt markets and offer higher return potential. They are ideal for long-term wealth creation and financial goals like retirement, children’s education, and financial freedom.

While FDs provide stability, Mutual Funds provide growth. For investors who want to grow their wealth and beat inflation, Mutual Funds are a smarter choice.